Climate Change and the Prime Swiss Alps Property Market: Are the “Big Names” Under Threat?

April 2026

The prime property market in famous Swiss Alpine towns and villages remains buoyant. According to Knight Frank’s Alpine Property Report 2026 [1], Swiss towns fill seven of the top 10 spots in Europe’s ranking of Alpine property prices per square metre, with Gstaad, St. Moritz, Verbier, and Zermatt all featuring in the top five. Andermatt and Davos, meanwhile, led the way in terms of price growth for the year to June 2025, with impressive increases of 14.6% and 10.5%, respectively.

Historically, the attraction of such locations has, of course, been closely associated with reliable winter snow conditions (alongside impressive ski infrastructure). Yet in recent years, climate change impacts on the traditional ski season have really begun to bite. Awareness of possible knock–on effects on the Alpine property market seems to be steadily increasing. For example, 47% of respondents to Knight Frank’s latest Alpine Sentiment Survey say they would always factor climate resilience into an Alpine property purchase decision [1].

It is therefore becoming increasingly crucial to go beyond general “Alps-wide” statements about climate change, towards more sophisticated and higher-resolution data able to resolve subtle differences from place-to-place, by season, and considering different plausible climate trajectories. Yet while much scientific data on climate and its change now exists, due to a lack of tools and interpretation, it has remained largely inaccessible to real estate professionals and buyers alike – and therefore rarely considered in actual decisions. SwissClimmo was established to provide precisely this kind of localised, scenario-based climate data.

Here we present an analysis of the localised data we have compiled at addresses across Switzerland [2] to assess past and possible future temperatures in a selection of the most prominent Alpine settlements, both annually and during the winter season. In particular, we explore whether Elevation Dependent Warming (EDW) [3] – the notion that higher elevations may warm more rapidly than lowlands in the same region – could affect the future growth and resilience of the “big names”, and thereby drive shifts across the wider market.

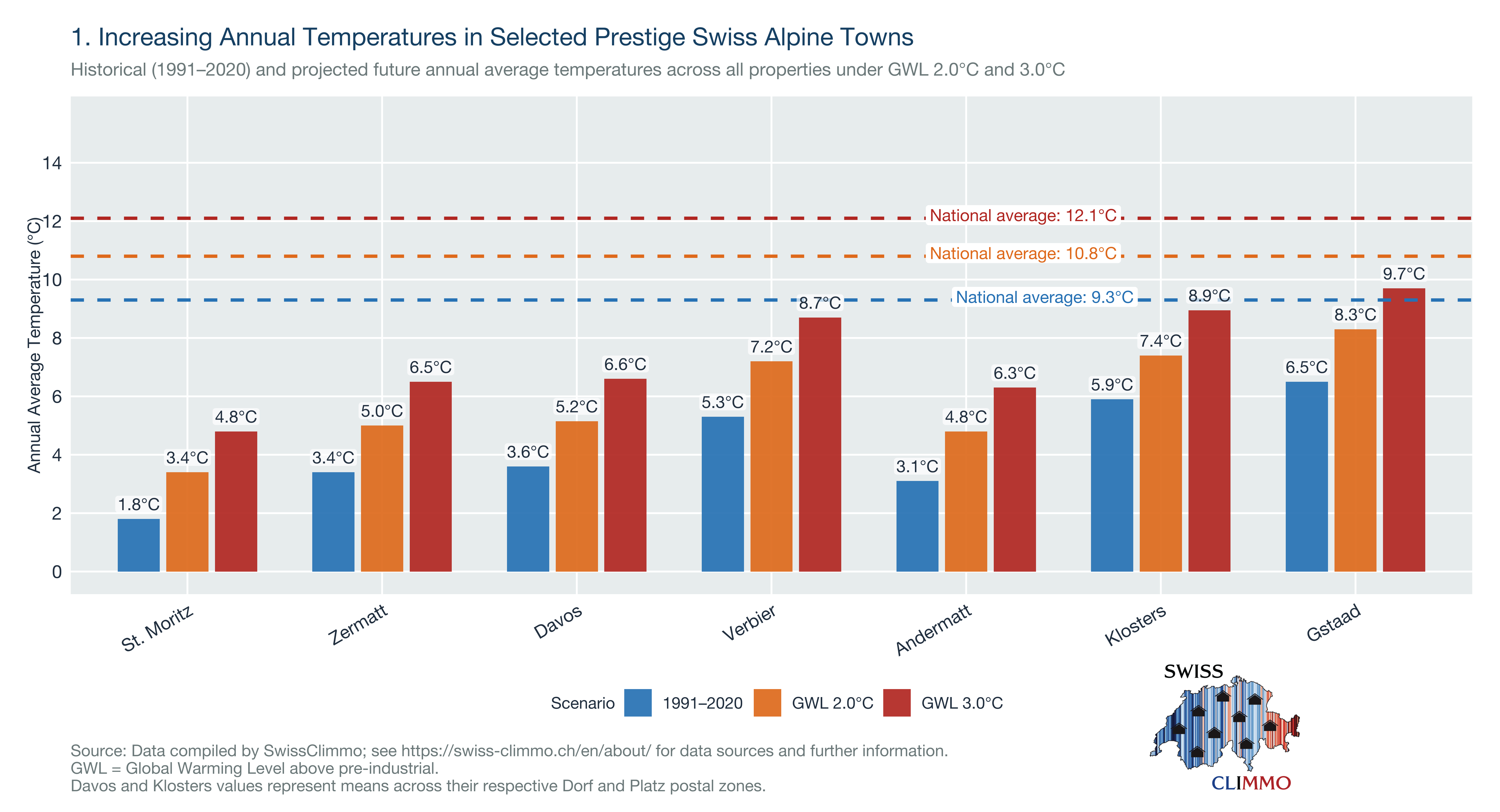

Over the historical reference period, annual average temperatures across properties in the six prime Alpine settlements have been significantly cooler than the Swiss national average (Figure 1), representing a key component of their established attraction. Under a Global Warming Level of 2°C (GWL2.0) (i.e. global average temperature 2°C higher than the pre-industrial period), increased annual average temperature of more than 1°C relative to the reference period are projected in each selected settlement. Importantly, the 1991–2020 reference period itself already reflects significant warming above pre-industrial levels. Further meaningful warming would be anticipated under a Global Warming Level of 3°C (GWL3.0). Indeed, temperatures in Gstaad would then surpass the historical national average.

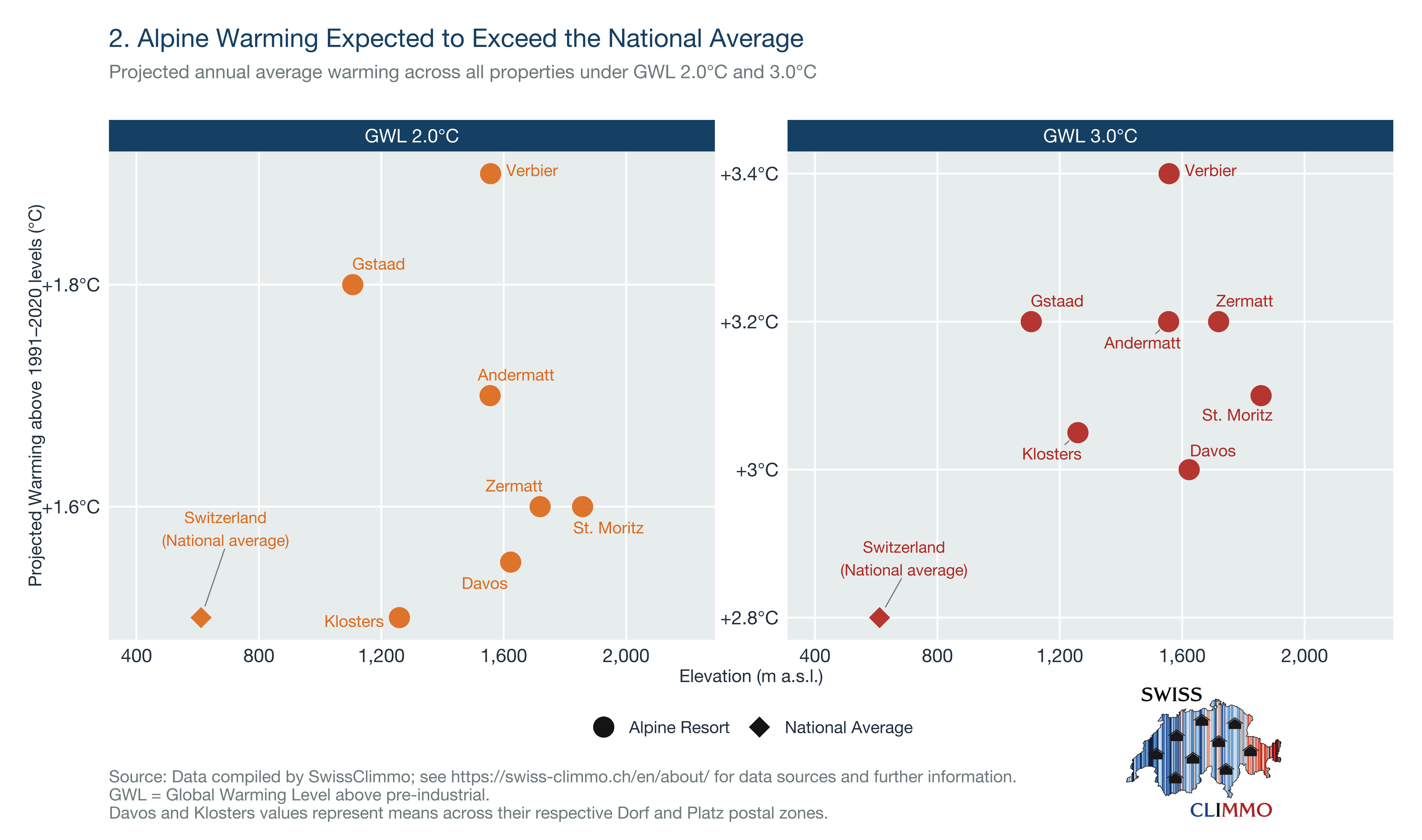

Warming across all of the Alpine settlements will either approximately equal (Klosters under GWL2.0) or else exceed (all other cases) the corresponding national average projected warming. When these temperature changes are plotted against the average elevation of the respective properties, the fact that the national average point sits below the Alpine cluster provides a clear EDW signal (Figure 2). Differences compared with the national average warming are especially pronounced under GWL3.0. Verbier appears as a major positive outlier under both scenarios, suggesting that its property market (and economy more generally) may be especially exposed to changing conditions.

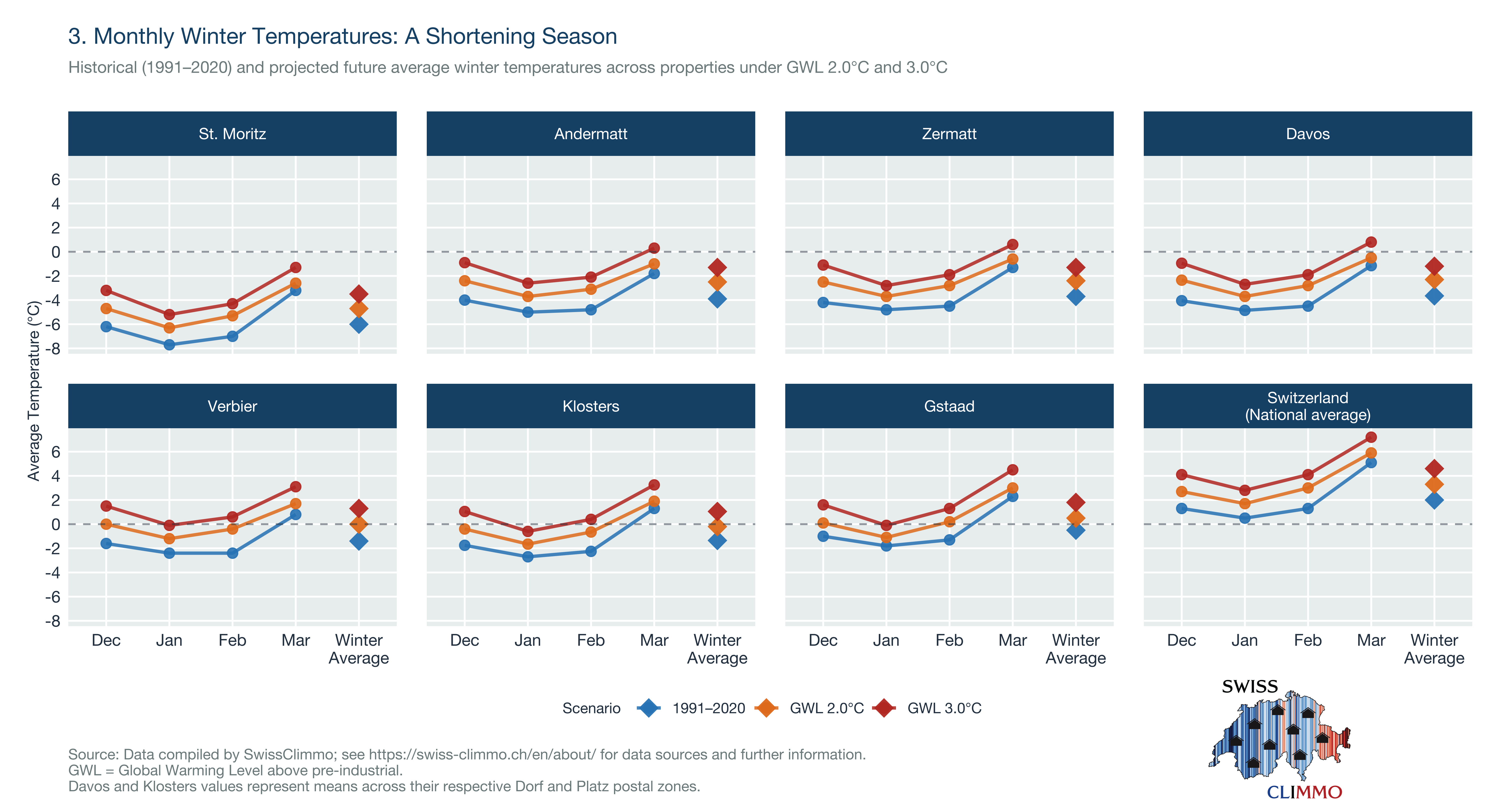

Temperature plots for the winter period only (December–March; Figure 3) show that, historically, all towns benefited from sub-zero mean temperatures across the core winter months of December, January and February. Such conditions contributed to a broadly reliable natural snow environment and attractive winter ambiance. However, in Verbier, Klosters, and Gstaad, average March temperatures were already positive historically, indicating somewhat marginal natural end-of-season snow conditions in and around lower elevation towns.

Under GWL2.0, December temperatures are expected to approach 0°C in several towns, potentially threatening the early-season period. Under GWL3.0, the situation will likely deteriorate markedly; warming temperatures in December and March could compress the traditional winter season in several resorts from both ends, with conditions in Gstaad probably becoming especially challenging. That said, being projected to remain sub-zero on average for most of the winter even under GWL3.0, St. Moritz, Andermatt, and Davos appear to have a “cold advantage”. Of course, shorter-term variability in temperature and changes in precipitation and other climate variables are also important to consider, but lie beyond the scope of this article.

Moreover, despite the pronounced expected annual and winter warming, the attractions that Alpine towns and properties will continue to offer remain numerous. Foremost are the ample opportunities they provide to pursue a myriad of other sport, leisure, and wellness activities, cooler summer conditions compared with increasingly sweltering major lowland cities, and better air quality (the latter two topics will be pursued in a future article). For these reasons, emerging trends towards greater emphasis on other seasons, year-round living, and places where traditional winter sports activities are secondary should continue.

Ultimately, all stakeholders in the prime Swiss Alpine property market must ask themselves questions such as: What will the Alpine towns property pricing ranking look like in 10 or 20 years time? Will established resorts be able to successfully adapt to the changing climate and retain their positions, or will there be new entrants into the top ten? In other words, which places will be “winners”, and which “losers”?

To explore a variety of climate metrics for properties across Switzerland, including uncertainties around future scenarios (not shown above), visit swiss-climmo.ch

Methodological note: Data presented represent simple averages across all properties within each postal zone. Where two postal zones exist for a single resort (Davos, Klosters), values represent the mean across both zones. Climate projections are expressed in terms of Global Warming Levels (GWLs) – that is, the climate state expected once the global average temperature has reached a given level above pre-industrial times – rather than specific future years, which would depend on the emissions pathway followed.

References

[1] Knight Frank Alpine Property Report 2026: https://www.knightfrank.com/research/report-library/alpine-property-report-12479.aspx

[2] SwissClimmo: https://swiss-climmo.ch/en/

[3] Pepin et al. (2022): https://agupubs.onlinelibrary.wiley.com/doi/abs/10.1029/2020RG000730